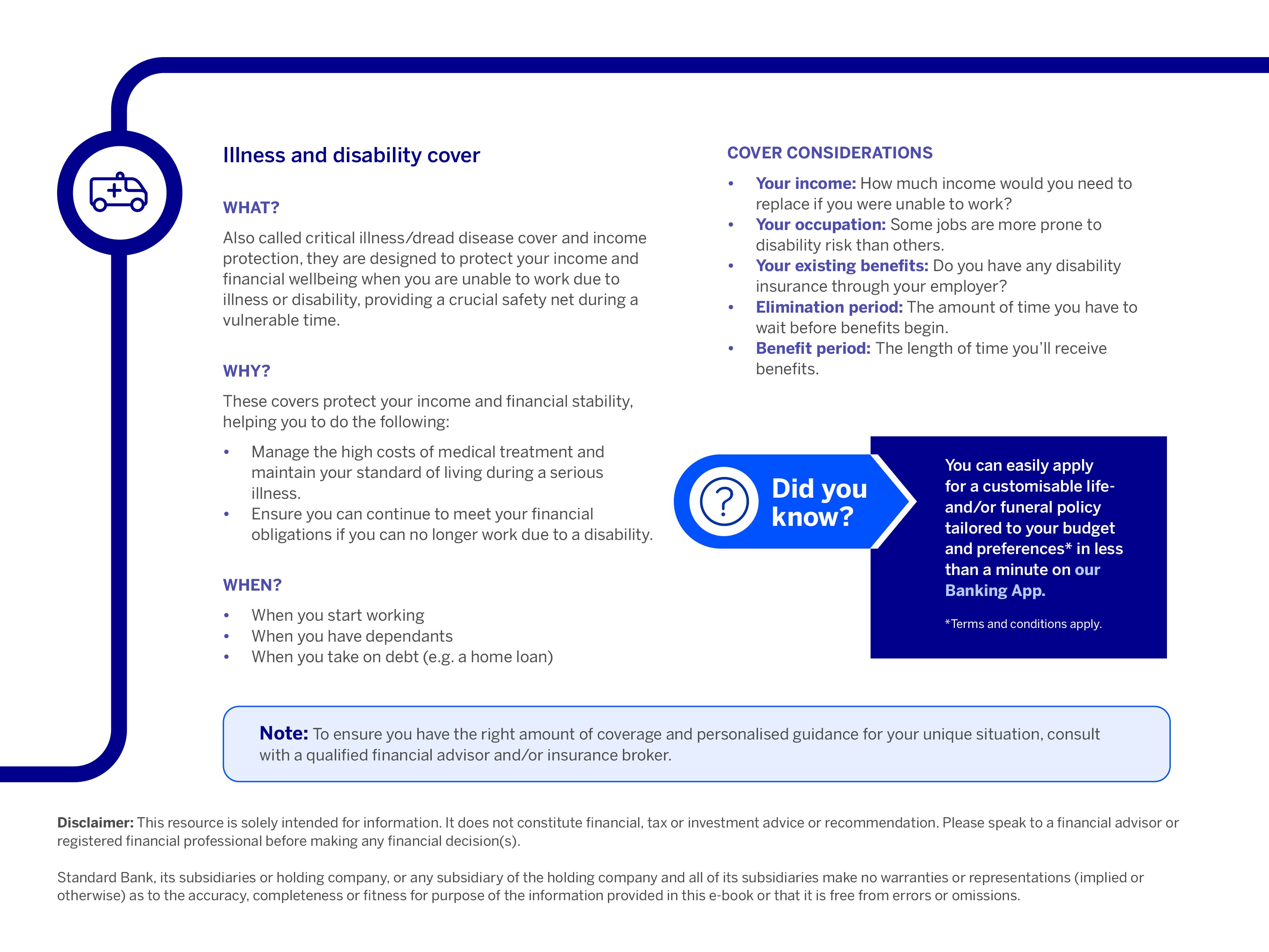

Guide to disability cover

Life is full of uncertainties, and sometimes, those unexpected turns can impact our ability to earn an income. Disability cover acts as a safety net to help you maintain your financial stability when your income stops.

Here’s a breakdown of what disability cover entails, how it works and why it should be an essential part of your financial plan.

What is disability cover?

Disability cover is a type of insurance designed to provide financial security and stability when you can no longer earn an income due to a qualifying disability, such as losing your eyesight or a limb or becoming severely ill.

One of your most valuable assets is the ability to earn an income, and if that’s taken away, disability cover steps in to replace it.

Why do you need disability cover?

Being unable to make a living can significantly alter your lifestyle and your family’s financial security. Additionally, if you do become disabled, you could likely also have more expenses (medical and otherwise), which you’ll need financial relief for.

Therefore, disability cover is crucial for the following reasons:

- It helps you continue to pay for essential living expenses (e.g. your rent or bond, utilities, groceries, and car and student loan payments), preventing financial hardship and debt

- Knowing you have the necessary financial coverage can reduce stress and help you focus on recovery and moving forward

- Disability can occur in various ways (both accidental and illness related), and having the right coverage can give you peace of mind

Who needs disability cover?

Disability cover is important for anyone who relies on an income to cover their living expenses, but it’s especially important for anyone who has dependants because not only can your standard of living be affected but also the current and future financial security of your loved ones.

If you have significant debt, such as a home loan, student loan or car loan, you’ll need to have a plan to cover those expenses. Disability cover also offers extra financial padding when you don’t have an emergency fund or only have limited savings, so you won’t have to dip into debt to survive.

What are common misconceptions about disability cover?

- Myth: “It won’t happen to me”

Fact: Noone is immune from the risk of illness or injury. Disability can affect people of all ages, professions and lifestyles, and often when least expected. Thinking you’re “healthy” or “lucky” can leave you unprotected against life’s uncertainties.

- Myth: “My workplace benefits are enough”

Fact: Many employers offer group disability benefits, but these often provide only a portion of your income, have strict definitions of disability, and may end if you change jobs. Relying solely on employer coverage might leave you exposed if your needs exceed what the policy pays. Personal disability cover can fill in gaps and ensure your income is truly protected.

- Myth: “I’ll always be covered by workmen’s compensation”

Fact: Workmen’s compensation only applies to disabilities arising from workplace injuries or conditions. If you’re injured outside of work, such as in a car accident or due to illness, these benefits typically don’t apply. Disability cover protects you from both workplace and non-work-related disabilities, offering broader financial reassurance.

How much disability cover do I need?

Disability cover replaces (a portion of) your income with a once-off lump sum, but determining the right amount of disability cover is a highly personal exercise as it depends entirely on your unique financial situation and future aspirations.

To get a clear picture, you'll need to assess your current monthly expenses, outstanding debts and all your financial obligations to understand what you'd need to maintain your lifestyle and cover essential living costs if your income stopped.

You also need to consider how your salary might have grown over time, the evolving needs of your dependants and your long-term financial goals. Balancing these needs with what you can realistically afford in premiums is key.

This is precisely why seeking professional guidance from a qualified financial advisor or insurance broker is invaluable; they can help you navigate these considerations and tailor a solution that truly protects your future.

Terms and conditions apply

Disclaimer: This article is for information purposes only and does not constitute financial, tax or investment advice. Readers are strongly encouraged to seek financial or legal advice before making any decisions based on the content.

Standard Bank, its subsidiaries or holding company, any subsidiary of the holding company and all of its subsidiaries, make no warranties or representations (implied or expressed) as to the accuracy, completeness, or suitability of the content of this article. The use of the article and any reliance on the content is at the reader’s risk.

Have more questions?

Download our free Insurance essentials e-book and learn more about the different types of insurance to help protect yourself and your loved ones..

Related articles and media