Your guide to insurance: Protecting family, assets and income

Life is unpredictable, and protecting yourself from the unexpected is an essential part of financial planning. Whether it’s ensuring your loved ones are taken care of, your home and car are secure or your income is protected, insurance acts as a safety net when things don’t go as planned.

With so many different types of cover available, understanding what each one does and when you might need it can help you make confident, informed decisions.

Here’s a guide to some of the main types of insurance, what they mean for you.

• Protecting yourself and your loved ones

Funeral cover

When dealing with the loss of a loved one, the last thing a family needs is to worry about how they will pay for the funeral. Funeral insurance provides financial support in the form of a lump-sum payment for immediate funeral-related expenses, such as a coffin, cremation and catering.

It ensures that families can say goodbye without the burden of unexpected costs or taking on debt.

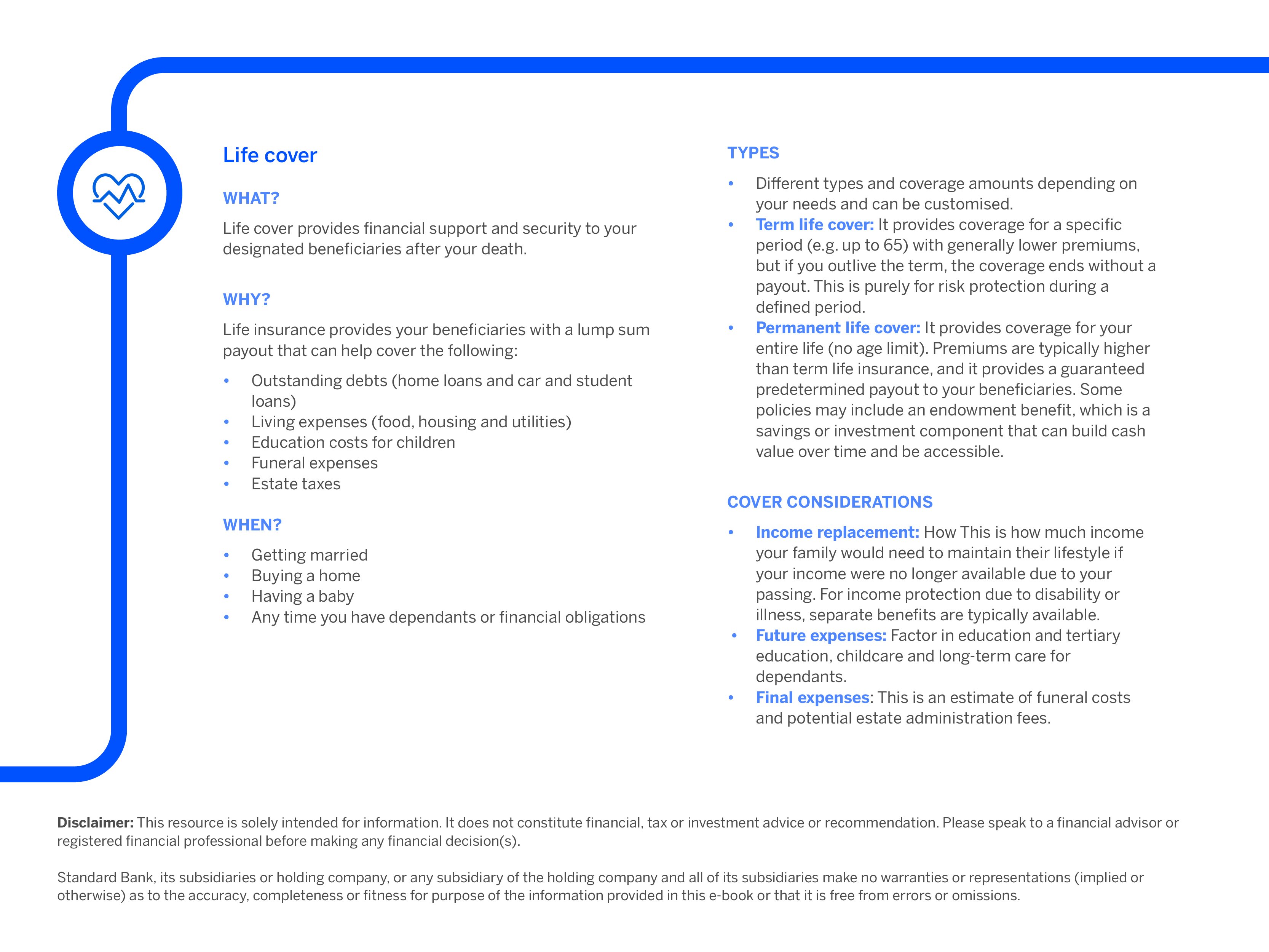

Life cover

Ever wonder how your family would manage financially if you weren’t around? Life cover, also known as life insurance, provides financial protection for your loved ones if you're no longer around. A lump sum payout can be used to settle debts, pay for living expenses, cover education costs or ensure your family maintains their standard of living.

Note that as your life changes, for example, you get married, buy a home or have children, it’s a good idea to review your cover regularly to ensure it still meets your family’s needs.

Personal accident plan

Accidents can happen when you least expect them. Accident insurance provides financial protection if you are permanently disabled or in the event of your passing as a result of an accident. It can help cover medical expenses, loss of income or other costs that arise while you recover.

This cover can be particularly useful for people who don’t have comprehensive medical aid or who work in environments with higher physical risks.

Explore personal insurance options to protect your family's financial wellbeing.

• Protecting your assets

Home insurance

When a sudden storm tears through your roof, a pipe bursts or you return home to discover your belongings have been stolen, the financial and emotional impact can be overwhelming. These unfortunate events highlight the critical need for home insurance which provides essential financial protection, shielding your home and its contents against a wide range of perils.

There are 2 types of home insurance:

- Building insurance: Covers the structure of your home against fire, floods, burst pipes or other disasters

- Home contents insurance: Protects your possessions inside the home such as furniture, appliances and valuables from theft, fire or damage

Car insurance

A sudden collision on the road or the unfortunate discovery of your car missing from its parking spot can instantly create a financial headache. Car insurance protects you against the costs associated with accidents, theft, fire and other damages to your vehicle.

There are 2 types of car insurance:

- Comprehensive cover: Covering loss or damage caused by collision, theft, fire or storms so that you can repair your own car but also covers damages you might cause to another vehicle or property.

- Limited cover: Third-party only, which only pays for damage you’ve caused to the other person’s vehicle in an accident, and third party and loss or damage from theft or fire.

|

Top tip Bundling your car and home insurance can lead to potential cost savings, discounts and simplified policy management with a single point of contact. A Standard Bank Insurance Brokers agent can simplify this process by providing up to 5 quotes from our insurer partners. |

• Protecting your personal and financial wellbeing

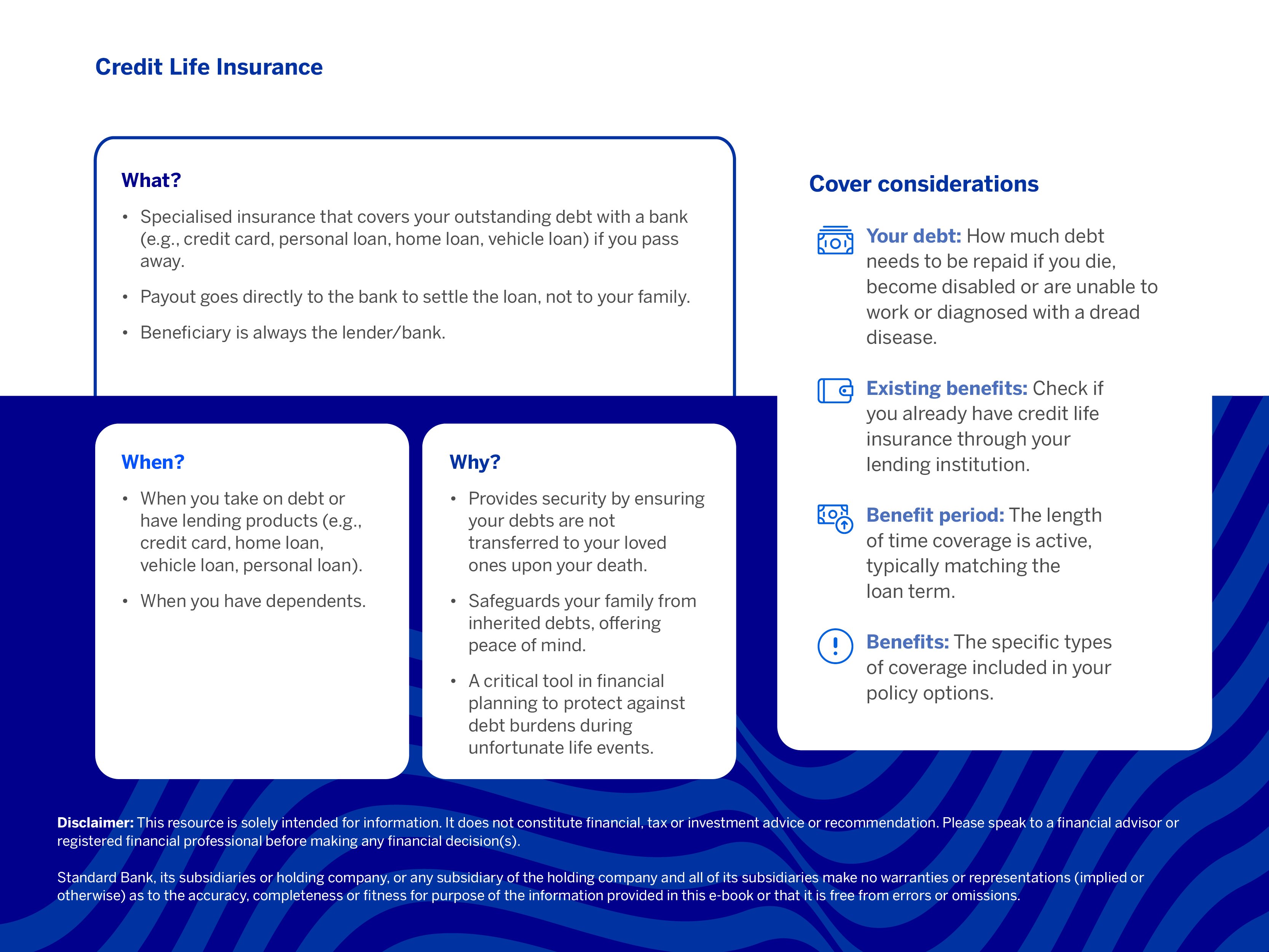

Debt insurance

If you have a home loan but could become unable to pay for it due to illness, disability or death, this cover ensures that your bond repayments continue for up to a year so that your family is relieved of the financial burden and potential loss of the home.

Many people don't realise that when you're no longer here or no longer able to pay your instalments due to illness or disability, your outstanding debts still continue and can become a financial responsibility your family has to manage.

Should the unexpected happen, debt insurance can provide your family with the funds to deal and manage with those debts and prevent them from further financial strain and the emotional burden of losing assets, such as a car or home, due to unpaid loans.

It includes credit card protection plans, loan protection plans, car shortfall insurance and car and asset finance protection plans.

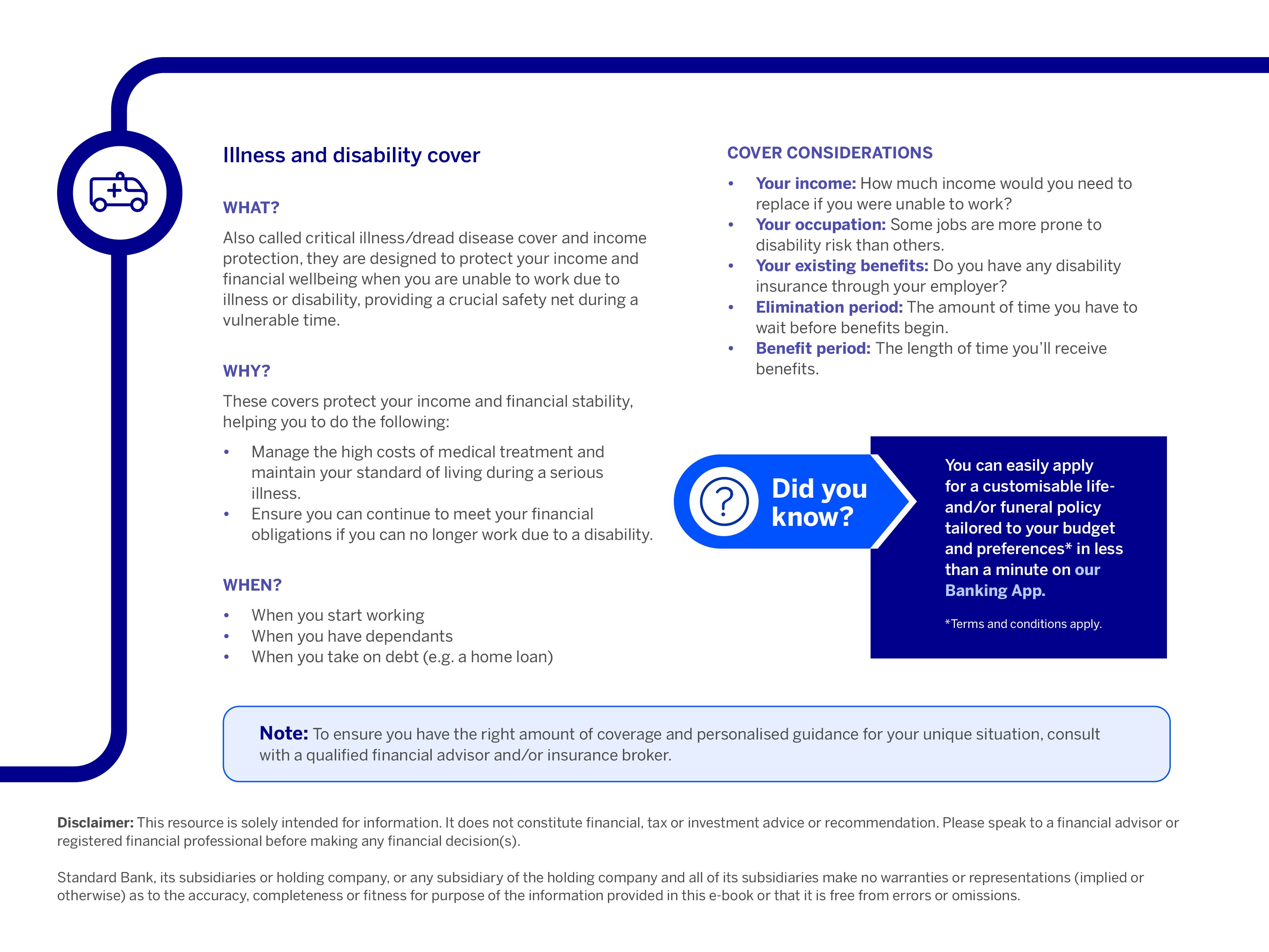

Income protection

Your ability to earn an income is a valuable asset, and if you were suddenly unable to make a living, it could have significant consequences for the wellbeing of you and your family. Income protection provides monthly or lump sum payouts if you’re temporarily or permanently unable to work because of illness or disability.

This type of cover helps your family maintain their standard of living and continue meeting financial commitments, such as paying your bond, school fees or other household expenses while you recover.

Travel insurance

Imagine you've meticulously planned your dream vacation, booked flights, accommodation, and activities, only for an unexpected event, such as a sudden illness, a family emergency or even lost luggage, to threaten to derail everything.

This is precisely where travel insurance steps in, covering a range of potential disruptions, from emergency medical treatment abroad and trip cancellations or interruptions to lost or delayed baggage and even personal liability, ensuring that if something goes wrong, you're not left to shoulder potentially high costs alone.

Remember, you get free* travel insurance when you purchase your tickets with your Standard Bank Credit Card.

*Terms and conditions apply

Disclaimer: This article is solely intended for information. It does not constitute financial, tax or investment advice or recommendation. Please speak to a financial advisor or registered financial professional before making any financial decision(s).

Standard Bank, its subsidiaries or holding company, or any subsidiary of the holding company and all of its subsidiaries make no warranties or representations (implied or otherwise) as to the accuracy, completeness or fitness for purpose of the information provided in this article or that it is free from errors or omissions.

Related articles and media