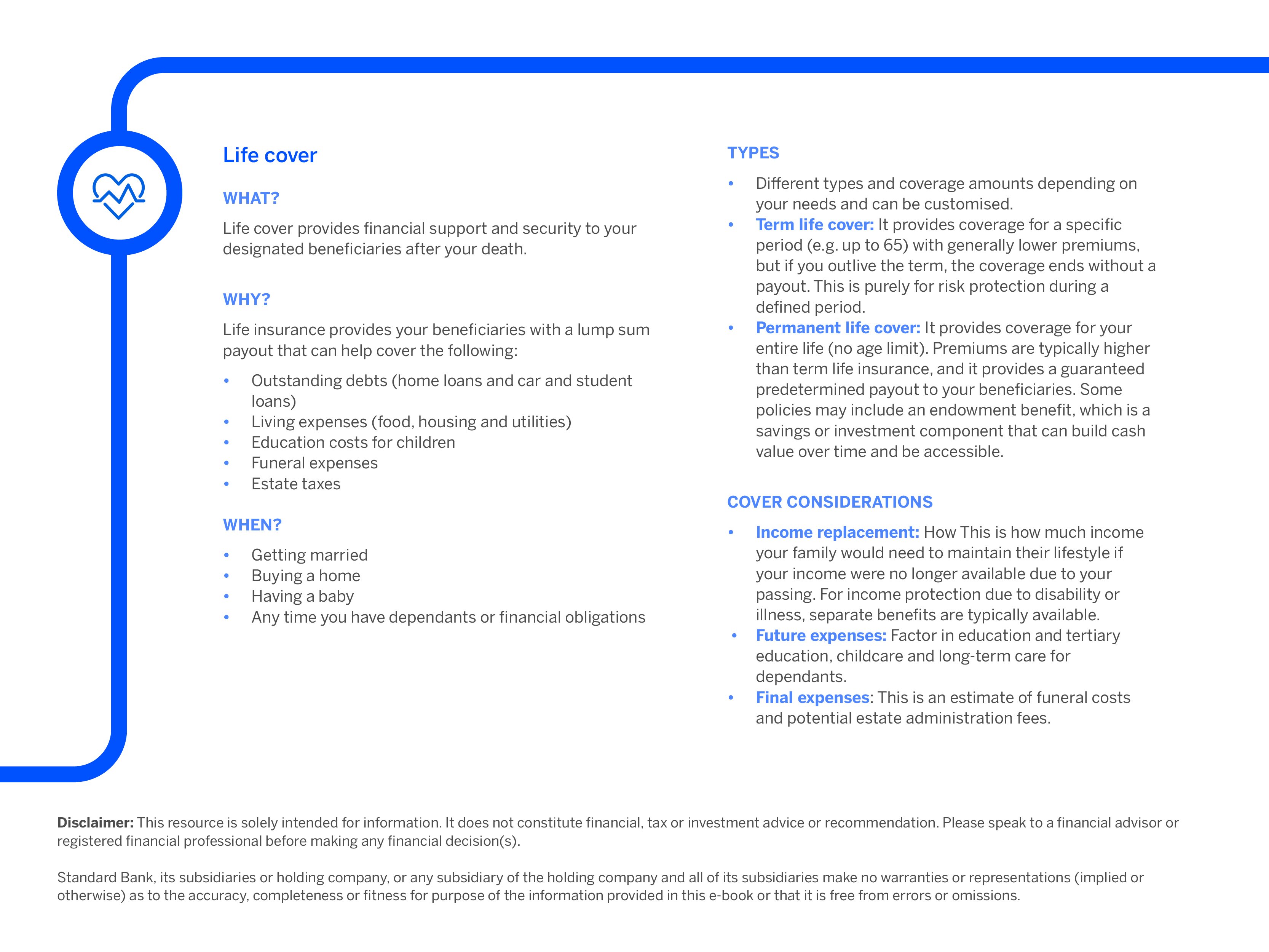

When to get life cover and why

For many of us, a significant part of our daily lives revolves around caring for loved ones who depend on us financially. Whether it's providing for a family, supporting elderly parents or ensuring the wellbeing of a dependant sibling, these responsibilities are real and deeply felt.

While we all hope to always be there, life's unpredictable nature means it's wise to plan for every eventuality. Life cover offers a practical and tangible way to ensure your financial support continues, even if you can’t provide for them directly anymore, providing stability and peace of mind for both you and those who depend on you.

Let’s explore the key reasons why and the best times to consider life cover as an essential part of long-term financial planning and wellbeing.

Why life cover matters for you and your loved ones

- Continued financial provision

Your financial contribution forms the foundation of how your loved ones live, supporting their daily needs and plans. Life cover can help ensure that this essential financial provision continues uninterrupted, even if you are no longer able to provide it yourself. It protects their ability to maintain their way of life and pursue their aspirations, preventing the added burden of financial struggle during an already difficult time. - Comfort in knowing provision is in place

For the policyholder, there's immense value in knowing you've secured your family's financial future. Should you pass away, your beneficiaries would receive a cash lump sum. This payout can help them cover essential living expenses, fund school and university fees, settle outstanding debts such as a home loan and maintain the quality of life you envision for them. - Delays can be costly

The best time to get cover is right now. You'll never be younger than you are today. As you age, your premiums will naturally increase. Delaying means you'll likely pay more for the same amount of cover later.

With age, the chances of developing minor or serious illnesses also increase. If you apply for life cover after being diagnosed with a significant health condition, your premiums could be substantially higher, or your illness might even be excluded from the policy, potentially preventing you from getting the cover you need.

When should I get life cover?

The best time to secure life cover is when anyone relies on your income or would face financial hardship in your absence. This often coincides with major life events, such as marriage, having children, buying a home or taking on significant debt (such as a home loan).

Key considerations in this decision involve the following:

| Financial needs of your dependants | Covering outstanding debts | Funding future expenses | Securing their everyday |

|---|---|---|---|

| Calculating how much income they would require | Providing for big loans (such as a home loan) that can influence their lifestyles | Providing for education | Ensuring their ongoing living costs are met |

- Even if you’re single, life insurance can cover outstanding debts (such as student loans or home loans) or funeral expenses or provide for aging parents or charitable causes. Securing a policy while young and healthy locks in lower premiums, offering a cost-effective way to protect your financial legacy and future insurability, even if your circumstances change later.

- If you're undecided, think about the financial impact of your death, even for minor costs such as funeral expenses. Securing cover now is wise because premiums rise with age and declining health; delaying could mean significantly higher costs or even being uninsurable if you develop an illness. While you can always increase coverage later, establishing a policy early locks in better rates and ensures eligibility.

Transform uncertainty into enduring care

Get flexible and customisable life cover that changes with your needs and your budget.

*Terms and conditions apply

Disclaimer: This article is solely intended for information. It does not constitute financial, tax or investment advice or recommendation. Please speak to a financial advisor or registered financial professional before making any financial decision(s).

Standard Bank, its subsidiaries or holding company, or any subsidiary of the holding company and all of its subsidiaries make no warranties or representations (implied or otherwise) as to the accuracy, completeness or fitness for purpose of the information provided in this article or that it is free from errors or omissions.

Want to know more about insurance?

Download our free e-book and get a better understanding of insurance, how it works and why you need it.

Related articles and media