7 Tips to improve your chances of getting a loan

When it comes to applying for a loan, there are things that help and things that hinder your chances of getting approved. Here are some tips on improving your chances before submitting and how you can avoid the risk of getting rejected.

To give yourself the best shot of getting your loan approved, it’s important to know some of the key factors that go into deciding whether or not a loan gets approved. Not only do these factors impact Having everything in order and knowing what needs to be fixed will help you plan ahead and put your best foot forward when applying.

1. Check your credit score

Your credit score shows your credit standing and behaviour, indicating how likely you are to pay back your debt. This determines whether you’re eligible for a loan and on what terms. Get your credit score in shape before applying for a loan.

Make sure all your bills are paid and fix any mistakes, such as incorrect information, that might appear on it. Also, keep the amount of credit you’re accessing low to show that you can sensibly manage money lent to you.

2. Approach the right lender

Just as there are different loans for different needs, different lenders have different requirements and approaches to risk. Be specific and realistic. Apply to a lender that’s a good fit for your needs and one that’s more likely to accept you.

3. Can you afford it?

An unaffordable loan isn’t in your interest, and it’s unappealing to lenders. Have you got a steady and reliable income, and do you have enough to pay the monthly instalments and cover your expenses? A bank or lender wants to ensure you’re able to pay back the money. Determine exactly how much you need, see whether you qualify for that amount and then apply for the minimum loan amount.

Use our personal loan calculator to estimate what you can afford.

4. Understand how the loan application works

The type of loan you’re applying for will determine what’s required to start and complete the process. Understanding what’s required, when it needs to be submitted and how long it takes, will help you prepare adequately and manage expectations accordingly.

5. Pay down existing debt

An important element of your credit score is your debt-to-income ratio: the amount of credit you used versus what’s available to you. A high ratio could indicate that you are overexposed to debt, impacting your chances of getting a new loan. Paying off debt will lower this ratio and make your application more attractive.

6. Consider collateral or a co-signer

If you’re having a hard time securing a loan, (depending on the loan type) you can put down collateral, showing the lender you’re serious and that you have incentive to pay back the money or risk losing that item of value.

Alternatively, if you’re just starting out or have a higher debt-to-income ratio, you can also ask someone with a good credit score or higher income to co-sign the loan application.

7. Be honest

Don’t stretch the truth. Overestimating your income, underestimating your debt or misrepresenting your employment could result in your application being rejected and a decline in your credit score. Reapplying or submitting multiple applications within a short period is also a red flag for lenders and makes them wary of approving your loan application.

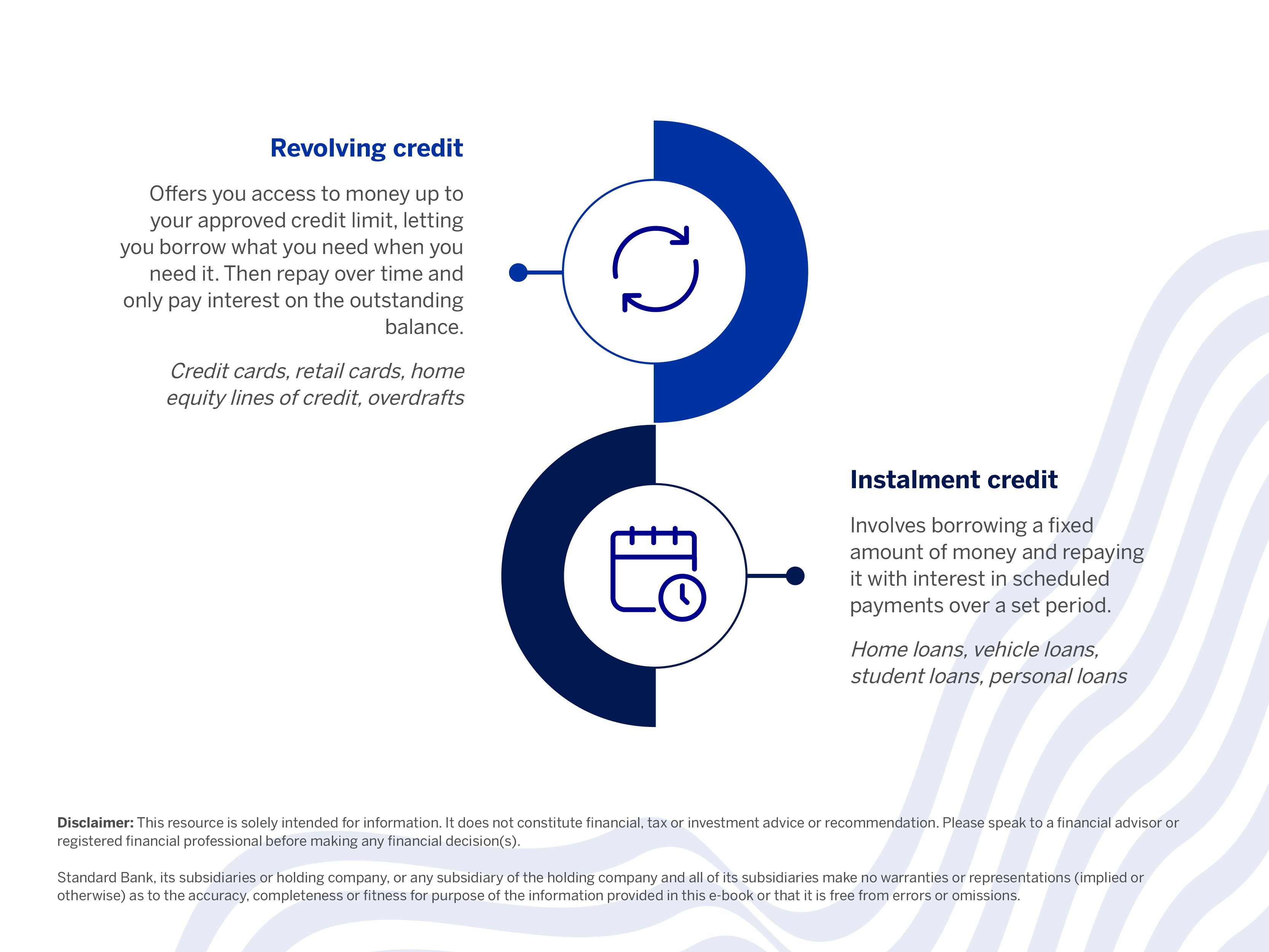

Different types of personal lending options available

Term Loan

Apply for a loan of up to R300 000* and pay it at a term you feel comfortable with.

Overdraft

Get access to additional funds when you need it most.

Revolving Loan

Unlock funds effortlessly with revolving credit.

Loan Consolidation

No need to juggle multiple payments. Combine up to 3 fixed-term loans into a single payment.

Credit made simple

Download our practical guide on how to use credit responsibly.

Terms and conditions apply.

Disclaimer: This article is for information purposes only and does not constitute financial, tax or investment advice. Readers are strongly encouraged to seek financial or legal advice before making any decisions based on the content.

Standard Bank, its subsidiaries or holding company, any subsidiary of the holding company and all of its subsidiaries, make no warranties or representations (implied or expressed) as to the accuracy, completeness, or suitability of the content of this article. The use of the article and any reliance on the content is at the reader’s risk.

Related articles and media