Investing offshore - Frequently asked questions

While there’s no guarantee that investing offshore will outperform local bets – investing out of the country is considered a key element when it comes to a balanced financial portfolio.

Investing in offshore markets is an important consideration for South Africans looking to secure their financial future through investment solutions. After all, South Africa represents less than 1% of the world’s economy, and limiting your investments to the local market means you’re missing out on possible lucrative opportunities to grow your wealth abroad.

Learn the basics of investing with our free Investment strategies for beginners e-book.

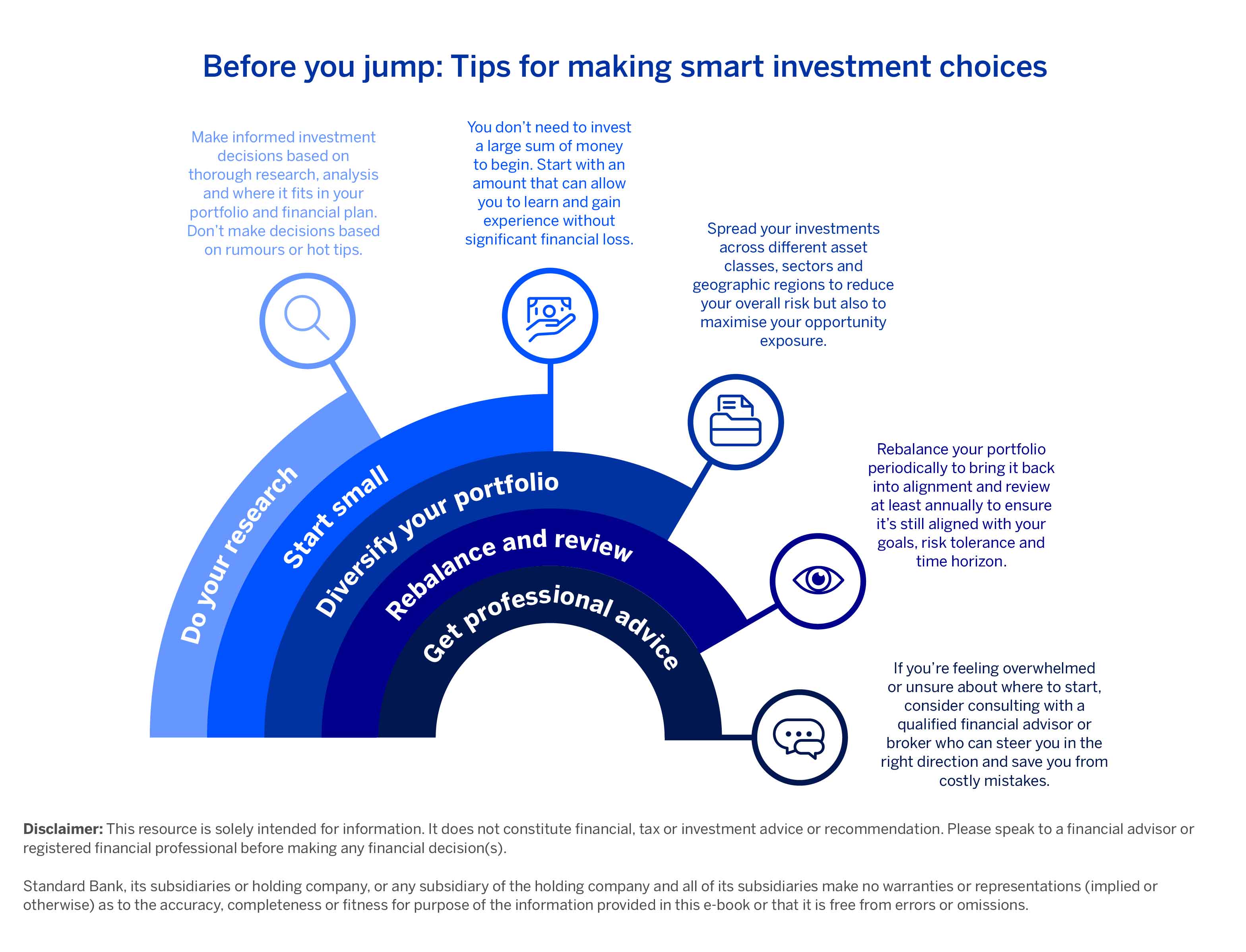

Investments offshore come with risks and benefits. Here are some pointers for how you can go about investing your funds offshore:

1. Why consider investing offshore?

Including offshore strategies in your savings and investment plan for the future is key to building a balanced yet diversified portfolio. Financial advisors will attest that if you limit your investments to South Africa, you’re essentially placing all your risk in one place. It’s the same for people in other countries, which is why foreigners invest in the South African market; they’re diversifying their portfolios.

Deciding to invest outside of the country could be daunting due to the sheer volume of international investments available, and navigating this landscape may be challenging – but it can be done, and the benefits truly warrant that investors take the leap.

The advantages of investing offshore:

- As a South African, offshore investment aids in capitalising on circumstances outside of the country, providing a buffer against our markets, our inflation spikes and our exchange rate fluctuations.

- But, there’s no guarantee that offshore investments will perform better than local ones as investment performance depends on numerous factors such as global economic conditions and exchange rates.

- Essentially, investing offshore allows you to achieve investment diversification. It enables you to access different economies and regions, as well as a broader selection of companies and emerging markets – increasing your potential to earn solid returns under varying conditions.

The risks associated with investing offshore:

- Developed economies may grow at a lower rate than South Africa, although at a lower risk. So, while global powerhouse markets like China, Japan and the USA can provide sustainable offshore returns, high-reward investment seekers might have to consider emerging markets.

- African markets are easily accessible, but you should research the continent in detail before you decide, so that you know what you are getting into. • Investing offshore unlocks global diversification, enabling access to different industries, interest rates and inflation circumstances, and stronger economies.

- Whatever your future concerns, as a South African serious about your financial wellbeing, you need to consider a portion of your total portfolio being invested offshore. Remember, however, that investing is a long-term game – five to seven years minimum.

2. What options for investing offshore are available to me as a South African?

For South Africans looking to diversify and build more balanced savings and investment portfolios for the future, there are two offshore investment paths to consider:

- Option 1 – Direct: Physically moving your savings or cash offshore by going through exchange control processes, opening up an offshore bank account in another country and sending your rand overseas in the currency of your choice.

- Option 2 – Indirect: Investing in rand-denominated investment options means your investment and currency exposure remain foreign, but you invest in rand and get paid out in rand because your money does not actually leave South Africa.

Option 1 – Direct: Physically taking your cash offshore

South Africans are allowed to take a maximum of R10 million a year offshore if they have been granted a SARS tax clearance certificate to move money abroad. Without this tax clearance certificate, you can only send a maximum of R1 million out of South Africa into your foreign bank account each year.

The R1 million transaction must be registered with the Reserve Bank. You would then need to place the transaction through an authorised dealer, which most South African banks are. Once the money is offshore, you may do with it as you please: leave it in the bank account in your name or invest it in unit trust funds or stocks in that country.

Option 2 – Indirect: Invest in foreign rand-denominated funds

There are several savings, investments and asset managers in South Africa that offer offshore unit trust funds. These funds are priced in rands, however, the capital is invested offshore, which provides global diversification and foreign currency exposure.

With this option, you aren’t obliged to obtain a SARS tax clearance certificate to invest in these funds as your investment is made in rand and paid out in rand on disinvestment. You are also able to set up a debit order and the lump sum minimums are a lot lower compared to moving cash overseas.

Another consideration is offshore ETFs (exchange traded funds). Once again you are investing in rand and will be paid out in rand.

3. What portion of a retirement annuity can be invested offshore?

If you are already contributing to a retirement annuity (RA), you probably have offshore exposure in your underlying investment choice. Regulation 28 of the Pension Fund Act governs how pension funds are to be invested, and the Act stipulates that a maximum of 25% of your money can be invested offshore in an RA solution.

4. How does investing offshore impact your estate?

Having investments offshore still forms part of your estate and you can be liable for estate duty in the jurisdiction in which you invest.

Certain South African investment providers offer offshore endowments which negate the need for probate (the process whereby a will is "proved" in a court and accepted as a valid public document that is the true last testament of the deceased) or an offshore executor. You may nominate beneficiaries which means that at your death the investment can either continue offshore or be paid out in foreign currency to the beneficiaries.

The tax advantages of using an endowment structure are also very beneficial as capital gains tax (CGT) is paid at a lower rate than for individuals and is calculated using the offshore currency, not rand.

Disclaimer: This article is for information purposes only and does not constitute financial, tax or investment advice. Readers are strongly encouraged to seek financial or legal advice before making any decisions based on the content.

Standard Bank, its subsidiaries or holding company, any subsidiary of the holding company and all of its subsidiaries, make no warranties or representations (implied or expressed) as to the accuracy, completeness, or suitability of the content of this article. The use of the article and any reliance on the content is at the reader’s risk.

Related articles and media