Best investment tips for beginners

Investing offers an incredible opportunity to grow your wealth over time, but for beginners, it can appear daunting with all the financial terms and strategies. The question is, how do you begin, and where do you go from there?

Once you understand the basics of investing, including factors that influence investment decisions and having a plan for managing both risk and rewards, you can start building a portfolio that balances safety, income and growth.

The difference between saving and investing

Many people get confused between what it means to invest your money and what it means to put money away in a savings account.

Saving is when you set aside money that you don't need right now in an account that grows by earning you interest. It involves little to no risk, lower returns and quick access to your money.

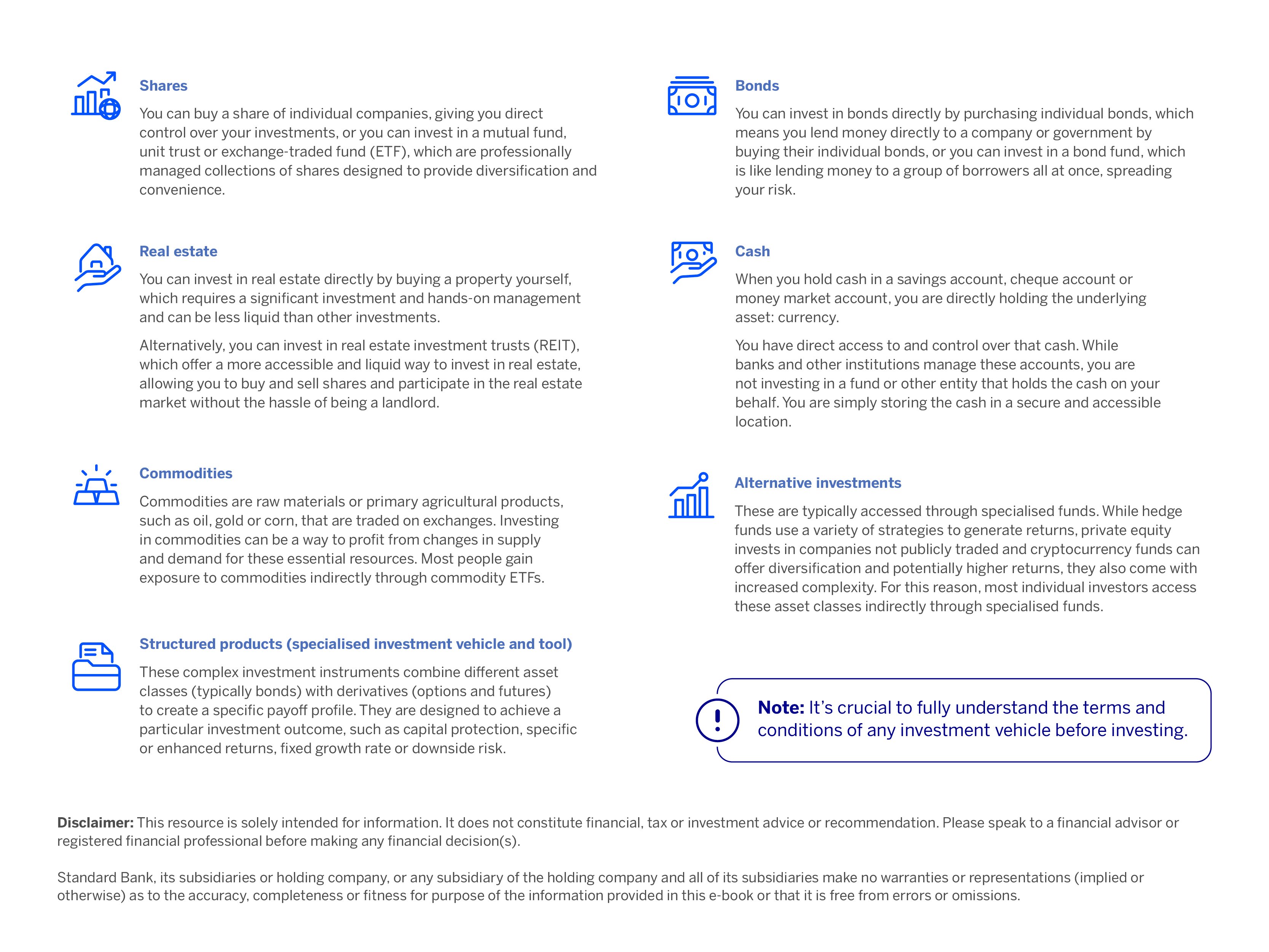

Investing is putting your money in something, i.e. buying assets such as shares, unit trusts or property, with the expectation that your investment will make money for you. Investments usually achieve long-term goals and can make your money work for you, helping you to create and preserve wealth.

Know your goals

Creating an investment portfolio can set you up for long-term financial success, but before making any investment decisions, including the type of account or investment you would like to make, it’s important to start by figuring out your financial goals.

What do you want to get out of the investment, and what do you want to achieve with that money?

To help you answer these questions and guide your next steps, before you start, answer the following:

- Why am I investing? (To buy a home, build a retirement fund, pay for my child’s education)

- What kind of returns do I expect?

- What portion of my net worth would I like to set aside for investments?

- What do I intend to use the gains for? How many years do I have?

- What is my investment objective? Is it capital appreciation, capital preservation or a combination of income and capital growth?

- What kind of risk am I willing to take in the long run?

1. Short-term vs long-term goals

It's important to know the difference between short-term and long-term investment goals and how they meet your unique financial needs. By aligning your investment decisions with the time you have, you can manage risk and maximise your potential for achieving your financial goals.

Short-term goals

- Need: Emergency fund, vacation, car downpayment

- Solution: Fixed income investments, such as unit trust funds, offer higher interest than bank deposits with relatively low risk. Compare rates before investing.

Long-term goals

- Need: Grow wealth over time (retirement etc.)

- Solution: Invest in assets such as stocks, bonds, mutual funds or property. Benefit from compound interest (earning interest on interest).

2. Income vs growth investment

A key decision in investment planning is determining whether you’re investing towards income or growth or a bit of both.

| Financial growth vs Income growth | |

|---|---|

| Investing for financial growth aims to increase the value of investments over time. This works well for long-term goals such as retirement. | Investing for income growth prioritises generating regular cash flow. These investments provide steady income, making them ideal for covering living expenses or achieving short-term financial goals. |

3. Matching your investment type with your goals

Saving is important, but to reach big goals, such as retirement, and outpace inflation, you'll likely need more than a savings account. While high savers (15%+ of income) can use savings as a starting point, exploring investments with potentially higher returns is crucial for long-term success.

Understanding the different types of investments and how they align with your objectives helps to match your investment expectation and results. For example:

- Cash and cash alternatives are low-risk options for short-term investing.

- Bonds offer fixed interest rates and can be invested in over the long or short-term.

- Stocks offer high returns but come with higher risk, making them better suited for long-term investments.

- Mutual funds offer diversification and potential growth, but management fees may apply.

- Exchange-traded funds are similar to mutual funds but trade on a stock exchange throughout the day, making them great for flexible investors.

Understand your risk tolerance

Your risk tolerance and the timing of your investment go together. If you don't take enough risk when saving for retirement 30 years from now, you might not save enough money. However, if you're only 5 years away from retirement and take too much risk, you could lose money and not have the chance to make it back.

Evaluate your risk comfort level using our risk tolerance questionnaire.

Download risk tolerance questionnaire

Your tolerance for risk is ultimately a balance between what’s required to reach your goals and how comfortable you are with market swings.

|

TOP TIPS FOR INVESTING

|

Ready to start investing?

Whatever your risk appetite, there’s an investment strategy for you. From conservative and cautious to aggressive and risky, there are plenty of options to choose from. The key is having a plan in place and doing research. With the right strategy and a little legwork, you can significantly increase your chances of reaching your financial goals through investments.

Open an investment account today and take the first step to building your wealth and financial future.

Disclaimer: This article is for information purposes only and does not constitute financial, tax or investment advice. Readers are strongly encouraged to seek financial or legal advice before making any decisions based on the content.

Standard Bank, its subsidiaries or holding company, any subsidiary of the holding company and all of its subsidiaries, make no warranties or representations (implied or expressed) as to the accuracy, completeness, or suitability of the content of this article. The use of the article and any reliance on the content is at the reader’s risk.

Investment strategies for beginners

Download our free e-book and get an introduction to investments and start growing your wealth with confidence.

Related articles and media