Back to basics: Interest rates

To navigate the world of finance, you need to speak the language.

Understanding the basics of common financial terms, such as interest rates, will help you make sense of how it’s applied and how it will influence your ability to reach your goals.

What is an interest rate?

An interest rate is how much it costs you to borrow money in the form of a home loan, personal loan, credit card or vehicle financing.

How do interest rates work?

Interest rates are calculated as a percentage of the amount you borrow over the lifetime of the loan. To fully repay a loan, you must pay off the loan amount and the percentage amount on top of the loan. This percentage amount is the interest you are charged.

For example, if you borrow R100 and you’re charged an interest rate of 5% per year (R5), the total amount you pay back is R100 + R5 = R105.

*This excludes certain fees that may be also added to the amount that you borrow.

Why do interest rates matter?

The interest rate you’re charged will affect how much the loan costs you (in total) and, therefore, how much you repay per month. Higher interest rates mean that it becomes more expensive to pay back money you owe, especially if you choose a longer repayment period.

The lender determines the rate at which interest is charged on the product (loan/credit). Some products have set interest rates, while others are personalised depending on your credit score.

If you have a low(er) credit score, the lender might consider it risky to lend you money and thus charge you more for borrowing it. The opposite is also true.

The maximum interest that creditors can charge you is determined by the National Credit Act.

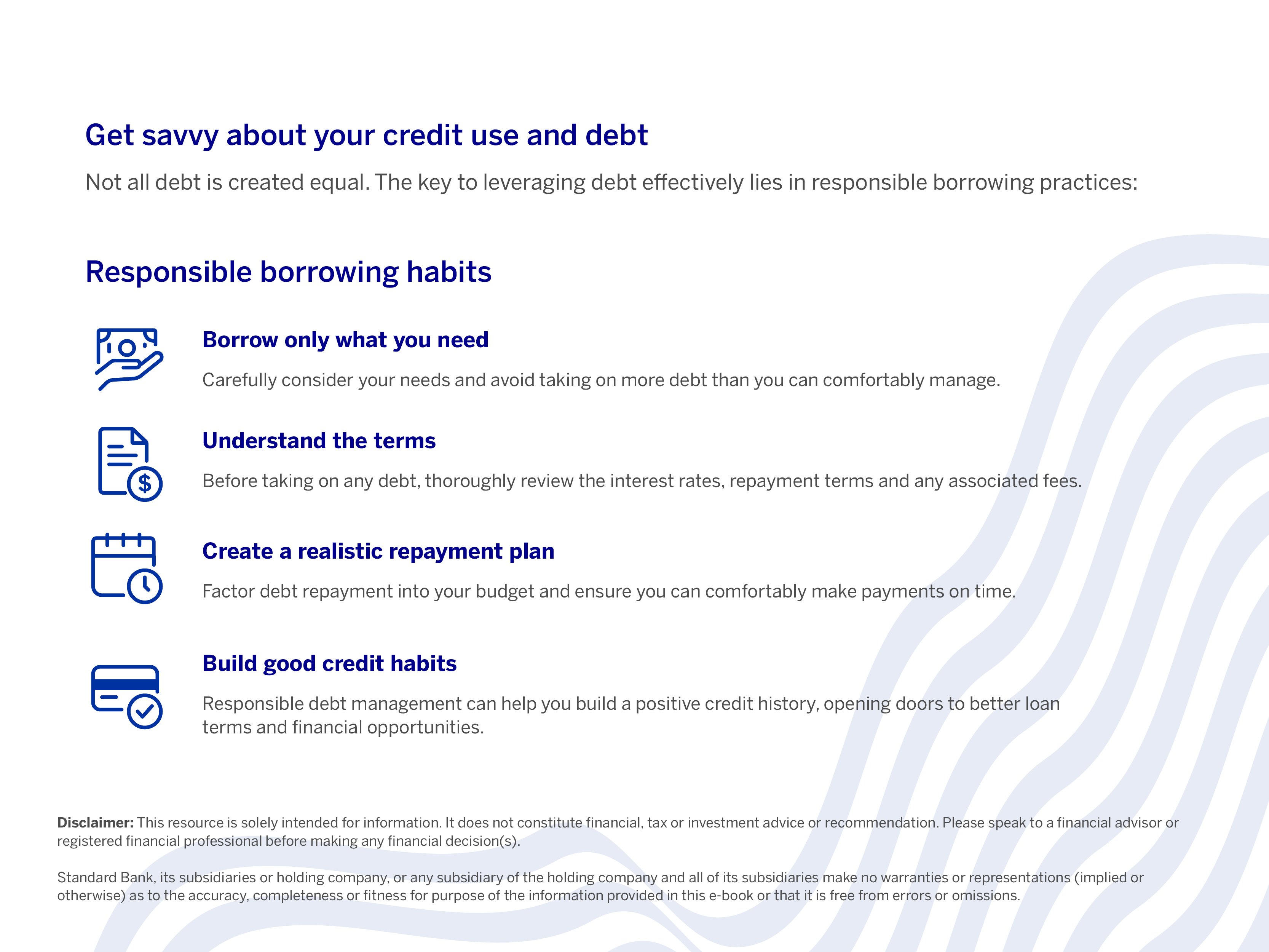

Before taking on any debt, thoroughly review the interest rates, repayment terms and any associated fees.

Learn more about what a credit score is and how it works and download our checklist to help you build a solid credit score.

The bottom line

Check your interest rate. When taking out a loan or accessing credit, consider how much you’re being charged to access that money. Being charged more interest will influence your ability to pay the money back, while earning more interest affects how your money grows.

Use credit responsibly

Download our e-book and learn how to use credit wisely to lower your interest rates.

Disclaimer: This article is solely intended for information. It does not constitute financial, tax or investment advice or recommendation. Please speak to a financial advisor or registered financial professional before making any financial decision(s).

Standard Bank, its subsidiaries or holding company, or any subsidiary of the holding company and all of its subsidiaries make no warranties or representations (implied or otherwise) as to the accuracy, completeness or fitness for purpose of the information provided in this article or that it is free from errors or omissions.

Related articles and media