Payday tips to make your money last

Waiting for payday can make the month feel much longer than it is, especially if you’re not sure whether your money is going to make it till the end of the month.

The good news is that careful planning and good spending decisions can help you stretch your salary without leaving you feeling stressed.

We’ve collected some of the best resources we have to offer and created easy tips and tricks to help you get started.

The 5 dos of making your money last

1. Prioritise your expenses

The key to managing your money is to know that you only have a finite amount of money, and how you spend it will affect how long it lasts. Start by identifying your essential expenses and setting money aside for these first. This ensures that your basic needs, such as housing, food and utilities, are covered.

Next, prioritise spending money and what you want to do with that money. Set aside an amount that you can spend comfortably to get/do the things you enjoy.

Creating a budget will help you plan and track your spending. You can download the budget template and learn some tips and tricks to help you save. You can also use the Budget Manager add-on in the Banking App to ensure you stay on track.

2. Keep track of your spending

Small purchases can add up to large amounts without you noticing. For example, do you ‘add to cart’ when you’re having a bad day, get tempted to buy the snacks while waiting in the queue to pay or tend to spend more than you planned on drinks at dinner and are then surprised when the bill comes?

Understanding your own spending habits and the type of things you usually spend your money on will help you avoid doing so or help you make better choices. Use our Money Movements add-on on our Banking App to help you stay on top of how you’re managing your money.

3. Create a spending plan with your family

Your budget plans could be derailed if your partner isn’t on the same page or if you’re constantly giving in to requests from your children. Include everyone in the plan and help them understand the (purpose of the) spending limits so they’ll have context when you say no and, hopefully, there’ll be less fighting about money.

- If you have kids under the age of 16, you can help them to grow up financially smart with resources designed specifically for them

- If your children are a little bit older, they can learn the essential money skills they’ll need to be financially independent

4. Change your mindset

Regardless of how you’ve managed money in the past, you can be in control and make positive financial decisions. It might not all change at once, but small and consistent changes can help you progress. This also includes being aware of challenges and how you approach your wants.

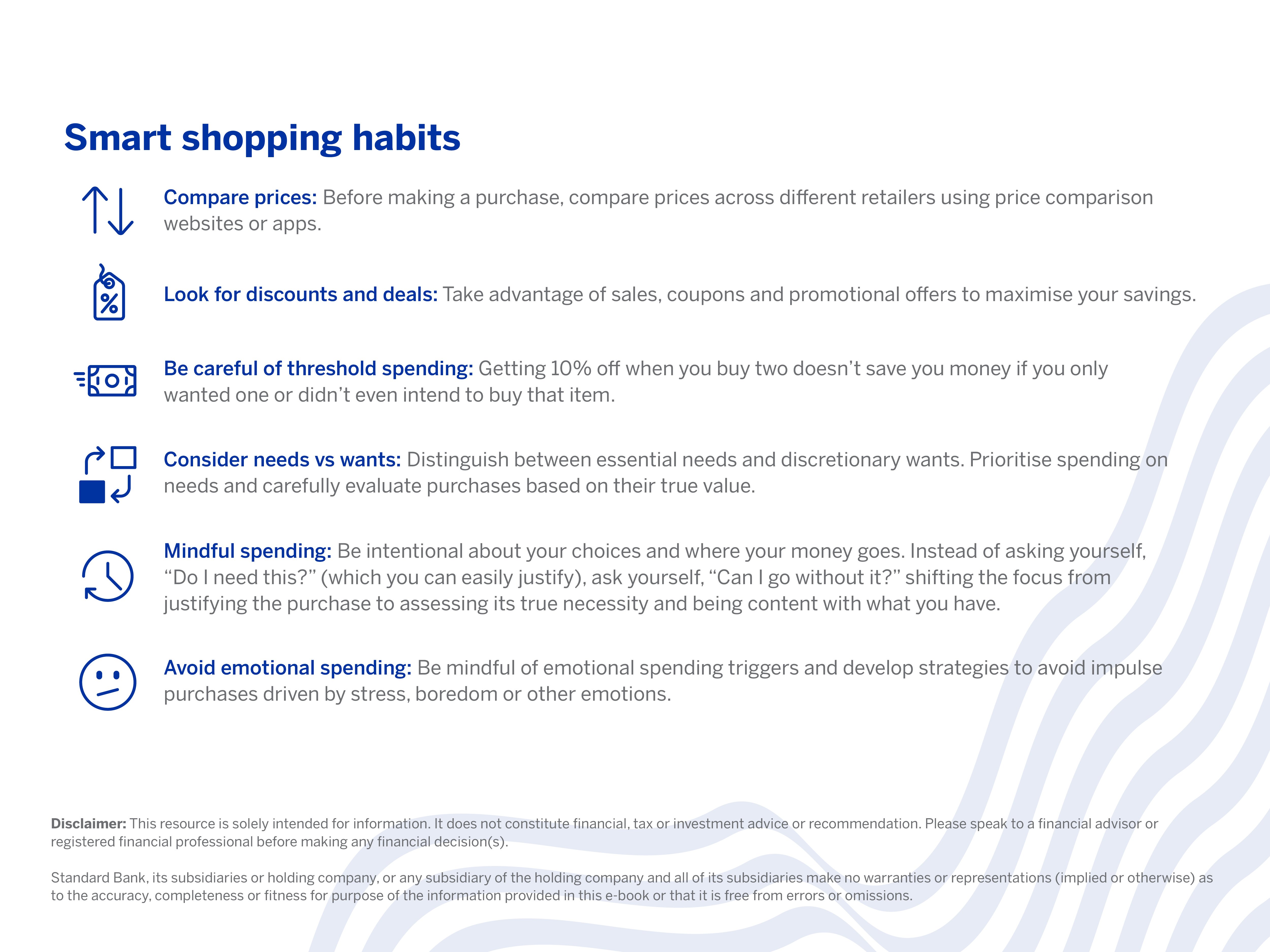

Instead of saying, “I don’t have money,” say, “It’s not a priority now,” or instead of saying, “I don’t need it,” when you have the impulse to buy something, rather ask yourself, “Can I do without it?” That way you’re not chastising yourself or being restrictive; you’re in control of your monetary decisions and prioritising yourself.

5. Have a financial goal

Whether it’s saving or paying off something, having a purpose for your money means you’re working towards a goal that is meaningful and you’re more likely to stick to it instead of just spending money without really knowing where it’s going.

You can use our short-term savings goal checklist to help you get started.

Short-term savings checklist

4 Things you can do to make your money last longer

1. Don’t go into bad debt

Consider using only cash or what is left in your bank account for a while. If you need to borrow, do so wisely. This could help avoid the opportunity to overspend, which will only cost you more later as the interest is an extra expense on every purchase.

Paying money towards debt takes away money that you could put towards essential expenses.

If you’d like to learn more about credit and how to use it responsibly, you can download our free e-book.

Download credit e-book

2. Don’t pay for things you don’t use (or don’t need)

Have a gym membership or streaming subscription you don’t use? Try to get rid of it. While you might have the best intentions, it’s taking up space in your budget, and it’s not serving you or your needs.

3. Don’t buy more to save more

Retailers entice you to spend more by giving you more savings if you buy more, but even if you get a discount, you’re still spending more than you intended to, and that’s an easy way to blow your budget.

One other way of overspending is to spend more to get free shipping. Do the math and work out whether it’s worth it to buy that extra item; either way, you end up paying for your free delivery.

4. Don’t shop without a list

Whether it’s at the store or online, plan ahead for what you need and stick to it. Aimlessly browsing can be fun, but it can also become expensive because you’ll walk out with things you don’t need or forget about the things you did, costing you more in the end.

Terms and conditions apply.

Disclaimer: This article is for information purposes only and does not constitute financial, tax or investment advice. Readers are strongly encouraged to seek financial or legal advice before making any decisions based on the content.

Standard Bank, its subsidiaries or holding company, any subsidiary of the holding company and all of its subsidiaries, make no warranties or representations (implied or expressed) as to the accuracy, completeness, or suitability of the content of this article. The use of the article and any reliance on the content is at the reader’s risk. .

Get savvy with your spending

Learn how to budget, set goals and make smarter financial decisions.

Related articles and media