The difference between savings and investments

Building a secure financial future involves making smart choices about your money and understanding what your options are. Whether you're dreaming of a new car, a down payment on a home or a comfortable retirement, understanding the difference between saving and investing is key. als.

They're both powerful tools for building financial security, but they serve distinct purposes and are best suited for different goals.

Think of it this way: saving is about keeping your money safe and readily available for immediate or short-term needs. It's about preserving what you have. Investing is about putting your money to work so it can grow significantly over time, helping you reach bigger, longer-term aspirations and building wealth.

Let's explore how these two financial strategies differ and when to use each.

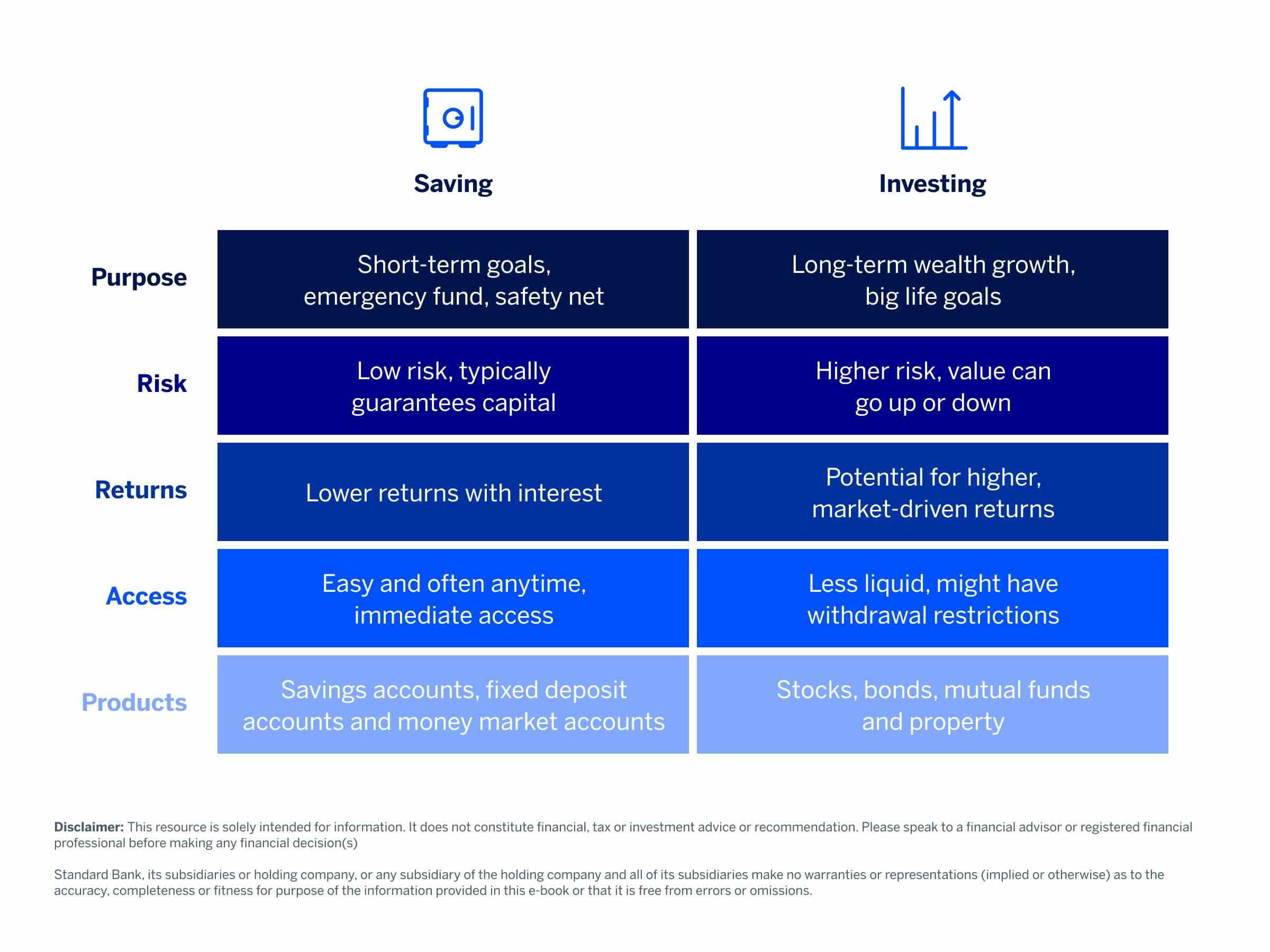

Savings: Your financial safety net

When you save, you place money in a secure account such as a savings account or fixed deposit with the primary goal of keeping your money protected and earning a predictable amount of interest. Savings accounts keep your money safe and provide you with access to it, making it ideal for the following:

- Emergency funds: That crucial 3–6 months of living expenses for unexpected events.

- Short-term goals: Things you plan to achieve within a few years, such as a holiday, a new appliance or a car down payment.

The peace of mind from knowing your money is secure and readily available is a significant advantage. However, savings accounts typically offer lower growth, with interest rates often struggling to keep pace with inflation.

Download our Savings strategies for beginners e-book today.

Download savings e-bookInvesting: Building your wealth

Investing involves using your money to acquire assets such as stocks, bonds or property, aiming for their value to increase over time. Its core purpose is long-term wealth creation. While it carries more risk than saving, it offers the potential for significantly higher returns.

Investing is crucial for long-term goals, those 5 or 10 years or even several decades away. This includes milestones such as retirement planning, funding a child's university education or accumulating substantial wealth. Over these longer periods, the power of compounding helps your money multiply and potentially outpace inflation.

However, investment accounts are subject to market volatility, meaning values can fluctuate, and there's always a potential for loss, especially in the short term. Therefore, your money isn't guaranteed to remain or grow, underscoring the importance of thorough research before investing.

Download our Investment strategies for beginners e-book.

Download investment e-book

Knowing when to save or invest

Deciding whether to save or invest isn't about picking one over the other; it's about understanding which tool best fits your specific needs. Ultimately, a robust financial plan (often) incorporates both saving and investing. They are complementary strategies that, when used wisely, can help you achieve your financial dreams.

For example, to ensure your financial wellbeing and ability to enjoy the things you like doing, you might maintain a healthy savings account for emergencies and short-term goals (such as a holiday) while simultaneously investing for your long-term aspirations (such as financial security and retirement).

To guide your decision, ask yourself these fundamental questions:

What is my goal?

Are you building an emergency fund, saving for a short-term purchase or planning for a long-term future such as retirement or a child's education? Your goal dictates the appropriate strategy.

When will I need the money?

If you need the money within the next 3–5 years, saving is generally a more efficient option. For goals that are 5 years or more away, investing offers the potential for greater growth.

How comfortable am I with risk?

Are you someone who prioritises absolute safety, even if it means slower growth, or are you willing to accept some market fluctuations for the chance of higher returns? Your risk tolerance will influence your strategy choice.

How accessible do I need this money to be?

If you anticipate needing quick access to your funds, a savings account provides that flexibility. If your money can remain untouched for many years, an investment account is designed for that long-term commitment.

Use our savings and investment product filter to help you find the best account options to match your specific goals and risk tolerance.

If you're unsure about the best path for your unique situation, speak to an accredited financial advisor to help you create a personalised plan to achieve your financial dreams.

Disclaimer: This article is for information purposes only and does not constitute financial, tax or investment advice. Readers are strongly encouraged to seek financial or legal advice before making any decisions based on the content.

Standard Bank, its subsidiaries or holding company, any subsidiary of the holding company and all of its subsidiaries, make no warranties or representations (implied or expressed) as to the accuracy, completeness, or suitability of the content of this article. The use of the article and any reliance on the content is at the reader’s risk.

Related articles and media