Understanding compound interest vs simple interest

Interest refers to the amount of money you can earn from the original amount in an account.

Given time, your money will grow based on the interest accumulated. There are 2 types of interest: simple and compound.

Interest-bearing accounts grow your savings exponentially through the power of compound interest. This means your money earns interest, which is then added to your balance. Future interest calculations are based on this new, higher amount, not just your initial deposit.

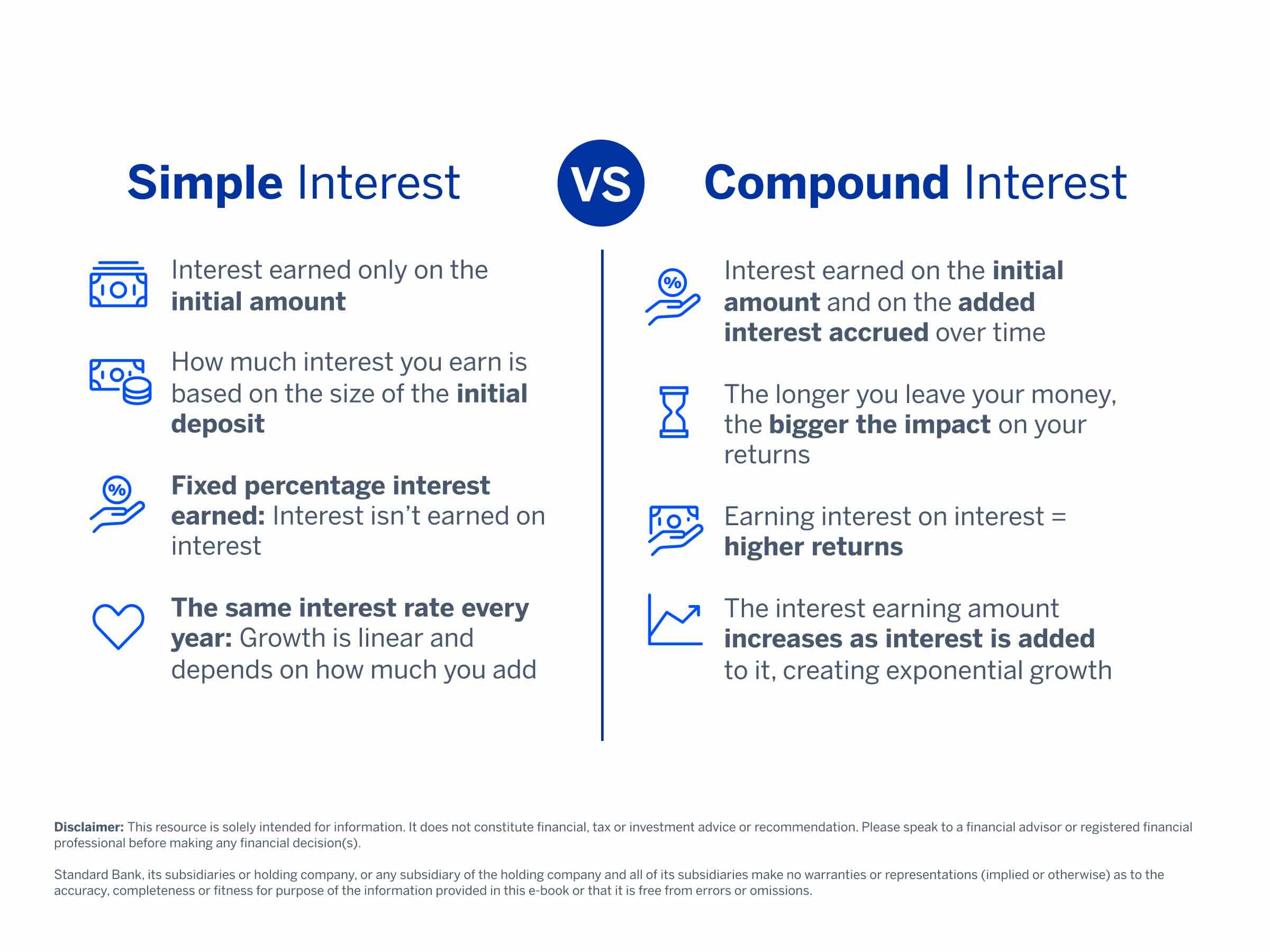

What is simple interest?

With simple interest, you earn interest based on an amount you deposit, which is calculated at regular intervals and will usually be applied and paid out at the end of the investment period. The percentage is always the same, and your money grows when you add more money because you’ll be earning that percentage of interest on a larger amount.

What is compound interest?

With compound interest, you earn interest based on the amount in your account for the calculation period, and the interest you earn is paid back into your account to increase the total amount you’re earning interest on. Simply put, compound interest lets you earn interest on top of your interest, causing your money to grow exponentially without having to add to it.

It's important to note that this distinction does not refer to changes in the interest rate itself but only to the amount on which you’re earning interest.

The power of compound interest

Compound interest is the secret weapon of long-term saving. It’s the process where your earnings generate even more earnings, creating a snowball effect that can significantly boost your savings over time. That’s because you aren’t just earning interest on your savings; you’re earning interest on the interest you’ve earned.

How it works:

If you put R1 000 into a savings account offering 5% annual interest, this could be what your growth looks like:

| Year 1 | Year 2 | Year 3 |

|---|---|---|

|

Starting balance: R1 000 Interest earned: R1 000 x 5% = R50 Ending balance: R1 000 + R50 = R1 050 |

Starting balance: R1 050 Interest earned: R1 050 x 5% = R52.50 Ending balance: R1 050 + R52.50 = R1 102.50 |

Starting balance: R1 102.50 Interest earned: R1 102.50 x 5% = R55.12 Ending balance: R1 102.50 + R55.12 = R1 157.63 |

Compound interest accelerates growth, so even if your contributions are small, they’ll add up substantially over time. You’ll also get to your goals sooner, and the longer your money is invested, the more dramatic the impact of compounding becomes.

Which is better?

Your investment goals and desired returns will determine which option is better suited to you. Generally, compound interest is a better option when you’re saving and investing since your money grows faster.

However, you need to look at the frequency of interest earned, i.e. how often the interest compounds. An account offering simple interest might offer a higher interest rate and longer investment terms, which means you’ll likely end up with more money in the long term, but you’ll have less access to your funds while they’re invested.

Successful financial planning is about choosing the right investment solution to suit your needs, and understanding the type of interest you’ll earn is essential to this decision.

How to grow your money

Where you house your savings will determine the rate that it grows at, but before deciding on a specific approach, think about what your specific financial goals and needs are. Think about what you are saving towards, how much you need for it and when you want it by.

Saving for short-term goals (less than 5 years)

1. Traditional/ Basic savings account

- What it is: An account designed to provide a safe and convenient place to store your money and earn a small amount of interest.

- What it’s great for: Putting money aside to start building an emergency fund or saving for short-term goals, such as a holiday or big-ticket purchase.

2. High-yield savings accounts

- What it is: Offers a higher interest rate compared to traditional or basic savings accounts, which means your money grows faster, allowing you to earn more interest on your deposits. Interest might be tiered based on your balance level, and they may have some restrictions, such as minimum balance requirements or limited access options.

- What it’s great for: Accelerating your savings growth and holding cash you may need soon; ideal for emergency funds and short-term savings goals, such as travel and down payments.

Learn how to start your emergency fund.

3. Money market accounts

- What it is: Money market accounts offer highly competitive, often fluctuating interest rates, tied to market conditions, with guaranteed capital and growth. They typically have minimum balance requirements and tiered interest rates and may incur fees if balances fall too low.

- What it’s great for: It’s a safe place to park your money and grow it with confidence and without risk. It’s good for growing a nest egg or growing money to put towards other investments.

4. Notice deposit account

- What it is: A notice deposit account is a type of savings account where your money is locked in a fixed period (days to years) at a predetermined interest rate. You have reduced access, and you must let the bank know when you want to withdraw. Penalties could apply for early withdrawals, but deposits are unlimited.

- What it’s great for: A lump sum of money that doesn’t need immediate access to; ideal for goals for which you can plan for withdrawal in advance, such as a down payment, a big celebration, educational goal or growing your money instead of letting it sit idle.

5. Fixed deposit account

- What it is: Fixed deposit accounts offer higher, guaranteed returns on a lump sum deposited for a fixed period. Longer terms typically yield higher interest rates, and access before maturity incurs penalties.

- What it’s great for: It’s ideal if you have a lump sum of money to grow and you don’t need immediate access to it, and it’s a good option if you are risk-averse and prefer guaranteed returns. A fixed deposit account is well suited to goals that you can plan for and that will happen soon, such as a down payment on a car, a wedding or home renovations.

Stay on track with your short-term savings.

Saving for long-term goals

1. Tax-free savings account (TFSA)

- What it is: TFSAs are long-term investment accounts offering tax-free growth and withdrawals, with an annual limit of up to R46 000 and a lifetime limit of R500 000. Exceeding these limits will incur tax penalties. To maximise growth and tax benefits, it’s recommended that you don’t access this money in the short term, leaving it as a long-term investment.

- What it’s great for: Every South African should have a TFSA as a savings supplement to other savings options, including retirement saving. It’s ideal to start contributing as soon as you can for yourself and your children; the earlier you start, the more time your money has to grow.

Learn more about tax-free savings accounts.

2. Retirement plans

- Retirement accounts (retirement annuities, pension funds and provident funds) offer tax advantages for long-term retirement savings, with specific rules regarding access. Choosing the right option depends on individual financial needs and goals, and each option has its own benefits and tax implications.

Learn how to set yourself up for retirement.

How do I know what type of interest I’m earning?

Simple interest applies when interest is based on a single investment amount for a fixed period, while compound interest is based on your balance.

Examples of compound interest accounts include our tax-free investment accounts, SaveUp account and Flexi Advantage investment account that offer the ability to make additional deposits or reinvest your interest earnings.

Our Fixed Deposit investment account is an example of a simple interest account, helping you grow your savings at a fixed rate for a specific period. Accounts like this might only allow for a once-off investment, pay out interest at maturity or offer the option of paying your interest into another account.

Disclaimer: This article is for information purposes only and does not constitute financial, tax or investment advice. Readers are strongly encouraged to seek financial or legal advice before making any decisions based on the content.

Standard Bank, its subsidiaries or holding company, any subsidiary of the holding company and all of its subsidiaries, make no warranties or representations (implied or expressed) as to the accuracy, completeness, or suitability of the content of this article. The use of the article and any reliance on the content is at the reader’s risk.

Want to learn more about saving?

Download our savings e-book to learn more about saving and how to get started.

Related articles and media