Understanding your credit score

Before you borrow money or take on more debt, ensure you understand what your credit score entails. Knowing the basics of this one financial term and how it affects your life will help you make informed financial decisions and, if need be, improve your financial health.

What is a credit score?

A credit score is a number system that shows lenders how creditworthy you are. It’s used as a gauge/indication of your ability to repay money you’ve borrowed, and therefore banks and financial institutions use it to see how risky it is to lend you money.

How does it work?

Your credit score is a record of how you’ve paid your bills. Do you pay on time, or do you miss payments? Do you manage your money well, or have you taken on too much debt?

Your entire credit history, i.e. anything you’ve borrowed money for or bought on credit (your cellphone, personal loan, credit card, vehicle financing etc.), gets calculated by the credit bureau to give you a number between 0 and 999. A higher score is better because it shows you can afford the credit.

Use our Banking App to perform a quick credit score check and continue to keep an eye on it to stay informed about your financial health.

How is your credit score calculated?

Your credit score is determined by a few key factors, and each factor carries a certain weight percentage. It’s important to note that different credit bureaus have different scoring models and criteria.

- Payment history (35 - 40%): What is your track record of paying on time and in full for your credit cards, loans and mortgage. On-time payments are positive for your credit score, and missed or late payments can negatively impact it.

- What you owe (30 - 35%): This looks at your total amount of debt: all of your credit cards, loans and home loans that you still owe on. This is used to see how you use debt and how often you dip into it. Owing a large amount that is close to what your income can be seen as risky and therefore, impact your score negatively. •

- Length of credit history (15 - 20%): This evaluates how long your accounts have been active and how long you’ve been accessing debt. If you have a longer credit history where you have demonstrated responsible use, it reflects positively.

- Types of credit (10%): Considering the combinations of different debt/credit types will indicate how you approach debt. For example, having secured, longer-term debt is more positive than only credit card debt and unsecured lending.

- Recent credit (10%): If you’ve opened accounts or applied for credit frequently in the recent months, this could indicate that you are having financial trouble and potentially risky to lend to, lowering your credit score.

Download your checklist for building a solid credit score.

Download credit score checklist

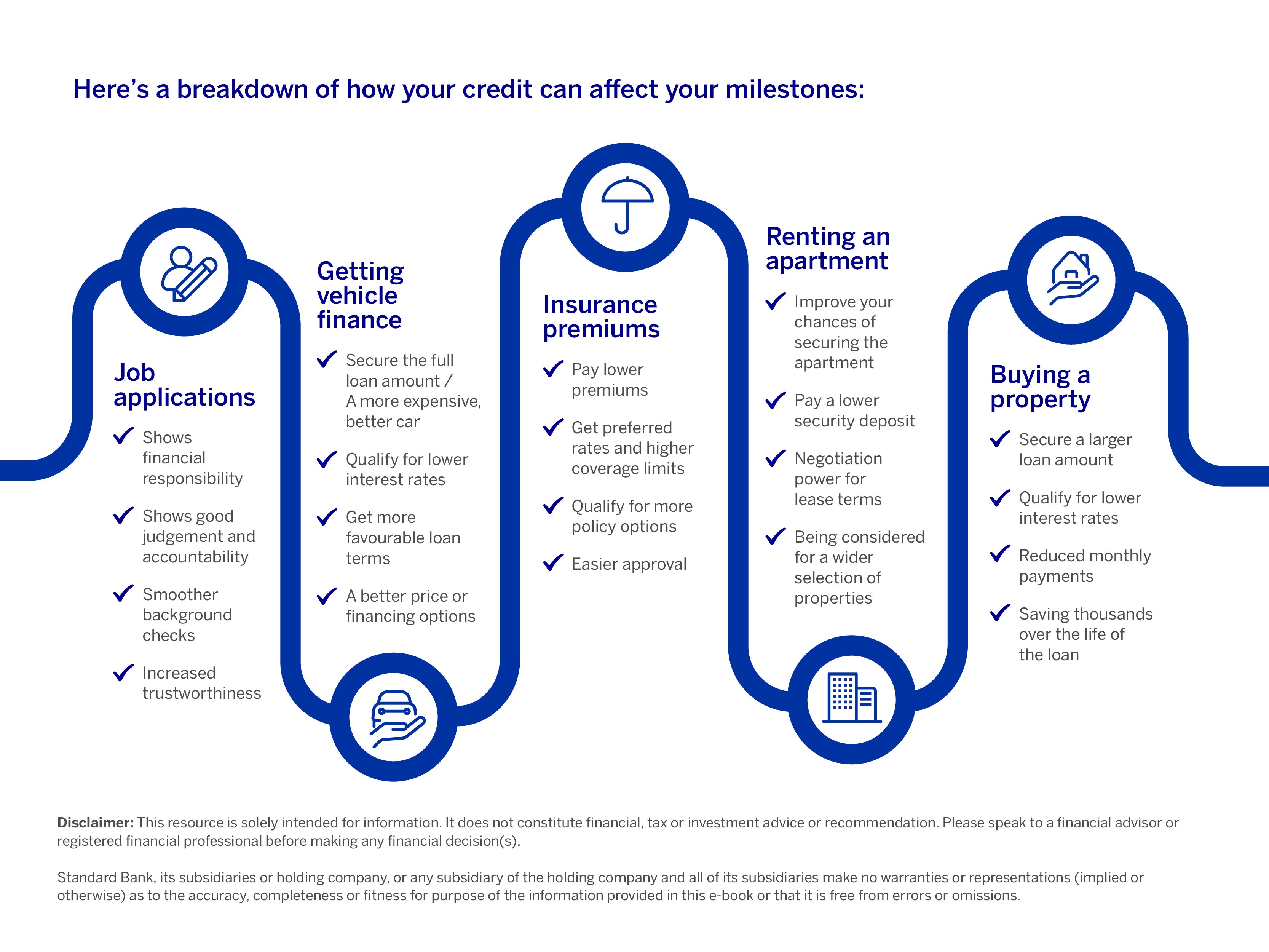

What is a credit score used for?

Whether you want to buy a house or a car or get insurance, your credit score is essential and will determine whether a lender gives you the money and at which interest rate. Different lenders have different lending criteria, and you may need a specific credit score.

For example, to apply for a home loan, you might need a score upwards of 600 (depending on the bank or financial institution) just to be considered. A higher score influences your chances of not only approval but also getting a favourable interest rate.

To increase your chances of getting a loan at a lower interest rate, you can take steps to improve your credit score.

Besides loan applications and credit approval, it can also be considered in the following scenarios:

- Renting a property: Landlords can use credit scores to assess how financially reliable you’d be as a tenant, and thus a better score would increase your chances of getting a lease. Having a lower score could see the landlord asking for a higher security deposit.

- Agreements for service contracts: If you want to get a cellphone or internet contract, your credit score might be checked before approving the agreement.

- Employment: For certain finance and sensitive industries, being creditworthy could be a requirement as part of the hiring process to indicate how financially responsible you are.

- Insurance: Insurance companies also look at how responsible you’ve been with your debt and, therefore, if you are eligible for lower premiums.

- Financial products and services: Your current interest rates are reviewed based on improved creditworthiness or accessing services, such as overdrafts or increased credit limits.

*Terms and conditions apply.

Disclaimer: This article is solely intended for information. It does not constitute financial, tax or investment advice or recommendation. Please speak to a financial advisor or registered financial professional before making any financial decision(s).

Standard Bank, its subsidiaries or holding company, or any subsidiary of the holding company and all of its subsidiaries make no warranties or representations (implied or otherwise) as to the accuracy, completeness or fitness for purpose of the information provided in this article or that it is free from errors or omissions.

Related articles and media